Insurance

How a lot does normal legal responsibility insurance coverage value?

There’s a spread of things that affect how a lot normal legal responsibility insurance coverage prices. We’ll stroll you thru them on this information

Common legal responsibility insurance coverage performs a necessary position in conserving companies financially protected if accidents involving shoppers and different third events threaten to derail their operations. That’s why it’s all the time advisable for firms to take out this type of protection no matter their dimension and the business they’re in. However how a lot does normal legal responsibility insurance coverage value?

On this article, Insurance coverage Enterprise crunches the numbers to learn the way a lot premiums value for such a coverage. We may also delve deeper into the components that have an effect on pricing and clarify how charges are calculated.

When you’re understanding how a lot protection what you are promoting wants and the way a lot this can value you, then you definitely’ve come to the precise place. Learn on and discover out all the pieces it’s worthwhile to learn about normal legal responsibility insurance coverage prices on this information.

The common value of normal legal responsibility insurance coverage for small companies ranges from $40 to $55 month-to-month or $480 to $660 per yr primarily based on the varied worth comparability and insurer web sites Insurance coverage Enterprise has checked out.

For the reason that dangers that firms face range enormously relying on a spread of things, their premiums will also be considerably greater or decrease than these figures.

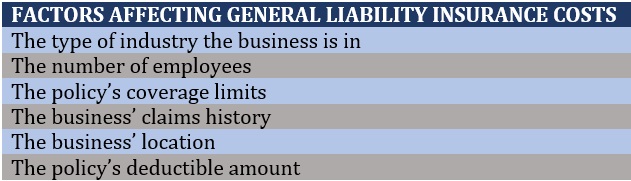

Whereas the estimated common value of normal legal responsibility insurance coverage our analysis discovered might not appear that top at first look, it’s essential to notice that the precise premiums a enterprise might want to pay might go nicely above or beneath that quantity, relying on the next components:

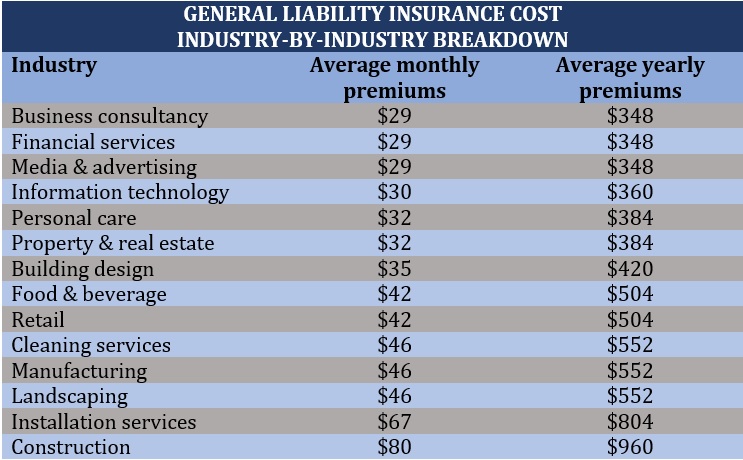

1. Trade

Totally different industries current various ranges of dangers which have a corresponding affect on normal legal responsibility insurance coverage prices. For instance, office-based companies that don’t expertise a number of foot site visitors equivalent to monetary and IT consultancies pay decrease premiums in comparison with retailers – which prospects frequent and face a higher chance of accidents.

One other instance is building and landscaping companies which pose a better danger of property injury.

The desk beneath lists the estimated month-to-month and annual premiums for normal legal responsibility protection for companies in numerous industries.

2. Enterprise dimension

The extra workers a enterprise has, the upper the price of normal legal responsibility insurance coverage. From an insurance coverage perspective, every workers member carries a sure stage of danger. A taxi fleet with 20 or extra drivers, for example, has a better chance of getting concerned in an accident in comparison with a transport service firm with 5 drivers.

3. Protection limits

In terms of coverage limits, there are two figures which have a huge effect on normal legal responsibility insurance coverage prices. These are:

- Per-occurrence restrict: The utmost quantity an insurer can pay out for a single declare

- Combination restrict: The utmost quantity an insurer can pay out in a yr

Per-occurrence limits are usually pegged at $1 million, whereas combination limits are often set at $2 million. These figures will be adjusted relying on the wants of the enterprise. The upper the bounds, the upper the premiums and vice versa.

4. Claims historical past

Every declare can increase normal legal responsibility insurance coverage prices come renewal time. Insurance coverage firms view companies which have confronted lawsuits and filed claims to cowl their losses as dangerous and can are likely to cost them greater premiums to offset potential future losses.

5. Enterprise location

Companies primarily based in areas with greater crime and accident charges usually tend to have costlier premiums than their counterparts in safer areas.

6. Deductible quantity

The deductible is the quantity that companies should pay out for an insured loss earlier than protection kicks in. Typically, the upper the deductible, the decrease the premiums because the insurer assumes much less dangers. If you wish to learn the way this insurance coverage element works, you’ll be able to try our complete information to insurance coverage deductibles.

Right here’s a abstract of the various factors that have an effect on normal legal responsibility insurance coverage prices.

Insurance coverage firms usually decide how a lot premiums a enterprise should pay utilizing a score system developed by completely different organizations, together with:

- Insurance coverage Companies Workplace (ISO)

- Nationwide Council on Compensation Insurance coverage (NCCI)

- North American Trade Classification System (NAICS)

- Normal Industrial Classification (SIC)

There are additionally some insurers that comply with their very own classification programs. What these score programs have in widespread is using class codes to find out how a lot danger a line of enterprise presents.

Aside from this, these codes – which include three to 6 digits relying on the scores company – allow insurers to establish what kinds of protection a enterprise wants or doesn’t want, to allow them to provide you with an acceptable pricing for the coverage.

Though normal legal responsibility insurance coverage insurance policies will not be that costly, there are nonetheless methods so that you can slash your premiums. These embrace:

- Buying a enterprise proprietor’s coverage (BOP): This kind of protection bundles collectively a number of insurance policies, together with industrial property, enterprise interruption, and normal legal responsibility insurance coverage, permitting you to save lots of prices than for those who take out separate insurance policies. BOPs, nonetheless, can be found solely to small companies with fewer than 100 workers and fewer than $1 million in income.

- Go for annual funds: Paying normal legal responsibility insurance coverage as one lump sum quite than by month-to-month instalments may end up in financial savings. Doing this helps what you are promoting keep away from being charged curiosity or finance association charges.

- Handle what you are promoting’ dangers: Having a spotless claims historical past is among the many greatest methods of conserving your normal legal responsibility insurance coverage value low. These will be so simple as conserving the ground of your institution dry to forestall individuals from slipping to implementing a complete security coaching program to your workers.

- Take note of mental property rights: Your enterprise will be sued for unauthorized use of photos, music, and different mental property. To stop this, just be sure you’re not committing copyright infringement, particularly when creating advertising or promoting supplies for what you are promoting.

Common legal responsibility insurance coverage – additionally known as enterprise legal responsibility or public legal responsibility insurance coverage – protects what you are promoting financially in opposition to claims of bodily damage or property injury ensuing from what you are promoting actions.

Most insurance policies additionally embrace product legal responsibility protection, which covers lawsuits from prospects claiming losses or damage due to a product you manufacture or promote.

Common legal responsibility insurance policies might likewise present protection for copyright infringement and incidents that trigger reputational hurt, together with:

- Libel

- Slander

- False arrest

- Malicious prosecution

- Wrongful eviction

- Invasion of privateness

If what you are promoting has been accused of inflicting these kinds of hurt, normal legal responsibility insurance coverage will cowl the authorized and settlement prices concerned. Such insurance policies may cowl medical bills incurred because of accidents that happen throughout the enterprise’ premises, no matter who’s at fault or whether or not a lawsuit has been filed.

Common legal responsibility insurance coverage isn’t legally required so that you can function a enterprise within the US. Nevertheless, some shoppers, stakeholders, and suppliers might make such a protection a situation for doing enterprise with you.

Though some companies face higher legal responsibility dangers than others, it’s all the time advisable to buy normal legal responsibility protection because it supplies monetary cushion within the occasion what you are promoting is sued due to an sudden accident. Common legal responsibility insurance coverage is a vital type of safety if what you are promoting:

- Has a retailer, workplace, or premises with heavy foot site visitors

- Sells merchandise or supplies companies

- Handles or conducts work for or close to a shopper’s property

- Makes use of social media as a part of your operations

- Creates commercials or advertising supplies for what you are promoting

- Wants protection to be thought of for work contracts

Every enterprise faces its personal share of distinctive dangers and challenges. Due to this, normal legal responsibility insurance coverage alone isn’t sufficient to supply full protection. Listed here are the opposite kinds of insurance policies that what you are promoting wants to make sure that you’re lined for any sudden incident:

- Staff’ compensation insurance coverage: A requirement in virtually all states, employees’ compensation insurance coverage pays out the price of medical care and a portion of misplaced revenue of workers who turn into injured or unwell whereas doing their jobs.

- Business auto insurance coverage: All industrial automobiles are required to hold such a protection for them to be legally allowed on US roads. It operates beneath the identical precept as private automotive insurance coverage, offering protection for third-party bodily damage and property injury ensuing from a collision.

- Medical health insurance: If what you are promoting has greater than 50 full-time workers, you might be required to take out medical health insurance to your workers, in response to the Inexpensive Care Act (ACA). However in case you have lower than 50 workers, you’ll be able to entry ACA’s Small Enterprise Well being Choices Program (SHOP) as protection.

- Business property insurance coverage: Additionally known as enterprise property or industrial constructing insurance coverage, this coverage is designed to attenuate disruption to what you are promoting’ day-to-day operations by offering compensation for damages or losses that occur to the property your organization operates in. This type of protection can also be usually a requirement for industrial leasing preparations.

- Skilled legal responsibility insurance coverage: Also referred to as errors and omissions (E&O) or malpractice insurance coverage, such a coverage protects what you are promoting from work-related claims, together with discrimination, mismanagement, and harassment. It additionally covers authorized and settlement prices arising from service-related errors and oversights.

- Administrators’ and officers’ (D&O) insurance coverage: This kind of enterprise insurance coverage is designed to guard the administrators and senior administration of an organization in opposition to monetary losses ensuing from business-related lawsuits. It pays out for financial losses ensuing from these authorized actions, together with protection prices, settlements, and fines.

- Enterprise interruption insurance coverage: Additionally known as BI or enterprise revenue protection, this coverage is designed to guard what you are promoting in opposition to monetary losses incurred from the disruption of your operations because of a lined peril.

- Cyber insurance coverage: Cyber insurance policies shield what you are promoting in opposition to monetary losses ensuing from cyberattacks.

Enterprise insurance coverage performs a significant position in offering what you are promoting with monetary safety from sudden occasions that may in any other case value you many 1000’s, if not thousands and thousands, in revenue, making it tough so that you can get better. If you wish to learn the way this type of protection will help you navigate tough instances, you’ll be able to try our complete information to enterprise insurance coverage within the US.

Given how a lot normal legal responsibility insurance coverage prices, do you suppose it’s a worthwhile funding? Is such a protection sufficient to guard what you are promoting? Be happy to share your ideas within the feedback part beneath.

Associated Tales

Sustain with the most recent information and occasions

Be part of our mailing listing, it’s free!